Terrifying Truth: How Terrorist Financing Really Works

Introduction: The Dark Reality of Terrorist Financing

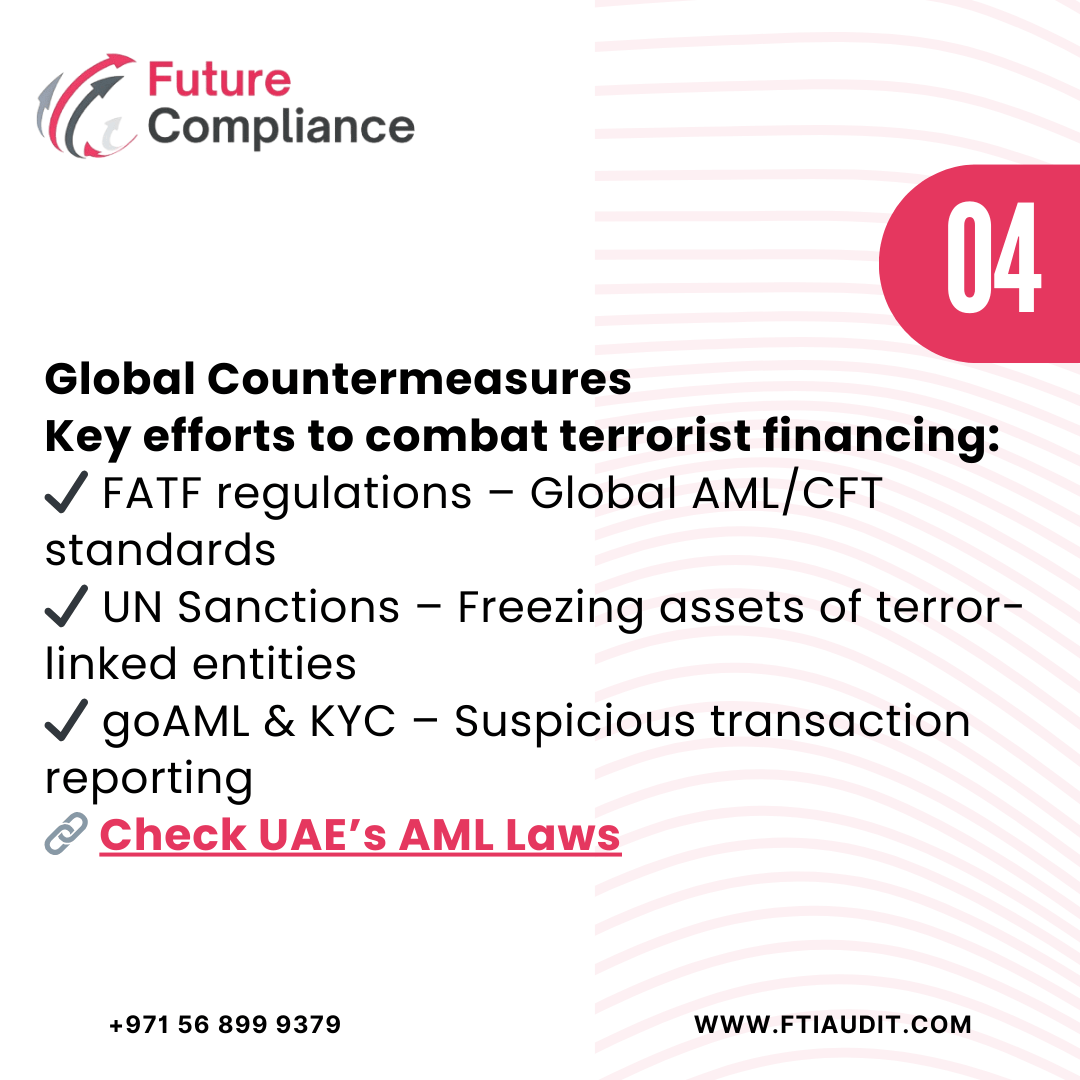

Terrorist organizations need significant financial resources to recruit operatives, execute attacks, and sustain their operations. Despite strict global countermeasures, they continue to exploit loopholes in financial systems to launder money and finance illicit activities.

Understanding how terrorist financing works is crucial for governments, businesses, and financial institutions to combat it effectively.

In this guide, we break down: ✔ Key methods used for terrorist financing ✔ Global regulations and countermeasures ✔ How businesses can prevent financial abuse

According to the Financial Action Task Force (FATF), terrorist financing refers to the collection, movement, or use of funds intended to support terrorism. Unlike money laundering, which seeks to disguise the origins of illicit funds, terrorist financing often involves both legal and illegal funds.

Once funds are raised, terrorist organizations use money laundering techniques to disguise their origins.

🔹 Placement: Introducing illicit funds into the financial system. 🔹 Layering: Moving money through multiple transactions to obscure its source. 🔹 Integration: Reintroducing funds into the economy as “clean” money.

How Businesses Can Help Prevent Terrorist Financing

If you’re a financial institution, DNFBP, or business handling international transactions, here’s how you can stay compliant:

✔ Know Your Customer (KYC): Verify identities and perform Enhanced Due Diligence (EDD). ✔ Monitor Transactions: Look out for unusual payment patterns, especially in high-risk jurisdictions. ✔ Report Suspicious Activities: Use platforms like goAML for Suspicious Transaction Reports (STRs). ✔ AML Training & Awareness: Conduct regular employee training on AML/CFT risks.

Conclusion: Strengthening Global Efforts Against Terrorist Financing

Terrorist financing remains a serious global threat, requiring coordinated efforts from governments, businesses, and regulators. Strengthening AML/CFT compliance, monitoring suspicious activities, and adopting international best practices are crucial steps in disrupting financial networks that support terrorism.

💡 Stay compliant. Stay vigilant.

For expert guidance on AML/CFT compliance and risk assessment, reach out to FTI Audit today!

For over 20 years, I have helped financial institutions improve their AML strategies. One major challenge is maintaining the accuracy of their risk scoring model in a rapidly data-driven world. Every day, countless transaction activities occur, making it essential to analyze multiple sources to detect financial crime risk. However, without strong data quality, even cutting-edge technology may fail to provide reliable risk evaluation.

Many organizations still depend on rules-based models for Anti-Money Laundering risk assessment. However, these models need constant fine tuning to remain effective. The rise of artificial intelligence (AI) and data science presents an opportunity to move beyond rigid rules. By developing a flexible framework, institutions can better respond to emerging threats. Adopting advanced methodologies and following industry best practices allows them to unlock their full potential in risk assessment.

Expert consulting and data-driven strategies can bridge the gap between traditional methods and AI-powered solutions. By evaluating different approaches and using aggregate data, institutions can improve the efficacy of their models. This enhances business relationships while ensuring compliance. A forward-thinking approach that blends human expertise with technology is the key to staying ahead.

Recognizing and Reducing AML Risks

When assessing AML risk, it’s essential to implement a systematic process that helps financial institutions identify and mitigate risks associated with money laundering and terrorist financing. By examining key risk factors and evaluating customer activities, institutions can get a clear image of their risk exposure. This is where a risk model comes into play, allowing institutions to calculate a risk score and identify high, medium, or low risks, ensuring that resources are allocated effectively to the highest priority cases.

An AML Officer plays a central role in this risk assessment process by ensuring that the risk rating aligns with the true risk level of each business relationship. Additionally, by proactively detecting and implementing proper controls, they can help manage the potential impact of financial crimes. Moreover, adopting risk-based strategies helps institutions prioritize efforts and reduce the likelihood of fraud. Ultimately, the goal is to be one step ahead by continuously assessing and fine-tuning the risk evaluation to prevent future money laundering risks.

The Significance of AML Risk Assessment

An AML risk assessment is essential for organizations to ensure they meet regulatory expectations and stay ahead of financial crime risks. By adopting a risk-based approach, institutions can efficiently allocate resources and apply enhanced scrutiny to high-risk customers. This not only helps prevent financial crime but also strengthens the integrity of the entire financial system. A strategic approach ensures both regulatory compliance and a commitment to safeguarding the system, making it easier to detect any potential threats. The thorough assessments conducted allow for a proactive stance in maintaining compliance and reducing risk.

Difficulties in Running an AML Risk Management Program

Managing an AML risk management program comes with key challenges like addressing financial risks and reputational risks. It’s important to take proactive measures and give careful consideration to ensure success. Only then can institutions ensure compliance and effectively tackle associated risks.

Data quality issues like inaccurate data can cause significant challenges in AML risk assessments. Transaction data and customer attributes must be comprehensive to ensure the assessments are reliable. When data is outdated or inconsistent, it may impede the accuracy of the risk detection process.

Many resource-constrained organizations struggle with managing the technological infrastructure necessary for continuous monitoring. This resource limitation impacts the ability to track changes in customer behavior and quickly refresh risk profiles, thus delaying real-time detection of potential risks.

External sources like adverse media and internal sources must be integrated properly to ensure a holistic view of customer behavior. Integrating data from different systems often presents challenges due to differences in formats, making it hard to perform comprehensive fraud detection.

The need for competent personnel and regular training can add to the complexity of running an effective AML program. Risk scoring models need to be well-designed and validated regularly to assess the risk exposure accurately and ensure that the AML risk assessment is robust and updated.

Screening against watchlists and analyzing transactions in real time requires constant updates of customer attributes such as occupation, industry, and transaction history. The infrequent data updates can result in an inability to detect fraud or assess risks accurately, compromising the overall system.

Real-time risk detection is critical for an effective dynamic AML risk assessment. If the system does not continuously refresh and update, it can fail to identify emerging risks. This is especially important when assessing risk profiles based on changes in customer behavior or external information.

Mastering the Art of an Effective AML Risk Assessment Framework

Building an effective AML risk assessment framework helps financial institutions stay ahead in compliance. It’s essential to align with regulatory requirements while continuously enhancing and improving the risk assessment process. This iterative process requires revisions and constant adherence to ensure institutional success and compliance.

Risk assessment is crucial for any institution aiming for robust compliance. Start by defining the scope and setting clear goals for the process. Choose a strong methodology and decide on the assessment frequency to keep track of the effectiveness of your framework. Assign the right responsible personnel and make sure available resources match the needs of your AML risk assessment.

Identifying relevant risk factors is the first step in designing a well-rounded framework. Consider the nature of your business, the demographics of your customers, the products/services offered, and the delivery channels used. Don’t forget to account for geographic locations, transaction monitoring alerts, and watchlist screening results. All of these play a role in the risk evaluation.

Data quality is key when performing an effective AML risk assessment. Collect data from internal sources like customer information and transaction data, as well as from external sources such as external risk indicators, typologies, and industry reports. This combination ensures completeness, helping you assess risk accurately while preventing data issues that can compromise the analysis.

Inherent risk assessment involves evaluating the probability and potential impact of risks related to money laundering and terrorist financing activities. By using historical data, industry trends, and regulatory guidance, you can determine the level of risk associated with each identified risk factor. This approach is integral in developing an accurate risk profile.

Creating a risk model involves quantifying risks through a structured risk scoring method. Assign risk scores or ratings based on likelihood and impact. This enables you to prioritize risks effectively and allocate resources where they are most needed. Both qualitative and quantitative factors should be considered in the scoring process for a comprehensive approach.

To ensure your program remains effective, implement risk mitigation measures. These could include customer due diligence, transaction monitoring, sanctions screening, staff training, and strong internal controls. Make sure these measures align with regulatory requirements and are tailored to the specific risk profile of your organization.

Monitor and review your risk assessment framework regularly to evaluate its effectiveness. Regular updates to your risk assessments are necessary to keep up with changes in your risk profile, regulatory landscape, and emerging risks. Maintaining a feedback loop ensures continuous improvement in your AML program.

Reporting is critical in AML risk management. Generate reports for management, regulators, and internal stakeholders to communicate risk exposure, mitigation actions, and the overall effectiveness of your AML program. Clear and concise reporting ensures that everyone stays informed and aligned with regulatory compliance.

Predicate offences are serious crimes that act as a foundation for illegal activities, including money laundering. These crimes work within an interconnected network, often triggering or protecting other criminal acts. To combat such threats, organizations follow international standards and adopt a strong regulatory framework. The impact of ignoring these offences can lead to financial instability and significant legal risks. Therefore, understanding how they are executed and what drives them is critical. Companies must apply best practices and stay compliant with relevant regulations. This approach helps them create a shield against risks and overcome associated challenges effectively.

What is a Predicate Offence? Definition and Example Explained Simply

A predicate offence is a crime that can trigger serious financial crimes, including money laundering or terrorism financing. These offences form a tangled web of illegal actions, often fueled by illicit funds from tax evasion or corruption. Gradually, these funds are converted into legitimate income, making it harder to track their true source. As a result, criminals successfully hide their illegal gains. Consequently, financial crime creates severe risks for the economy, making it a top concern for global regulators and enforcement agencies.

Understanding Predicate Offences in Money Laundering

Money laundering hides the source of money earned through a predicate crime or other criminal activity. These predicate offences serve as the basis for laundering proceeds of crime, such as illicit gains from human trafficking or other illegal activities. To counter ML/TF, governments worldwide have criminalised these offences. Moreover, local and international bodies have classified 21 major predicate offences to improve regulation. Since money laundering is rarely done in isolation, focusing on the underlying crimes is essential for prevention.

Understanding Predicate Offence under UAE AML/CFT Laws

What is a Predicate Crime? Explanation under UAE Laws

Under UAE laws, a Predicate Offense refers to any act that qualifies as a felony or misdemeanour. This crime can be committed inside or outside the country but must be punishable in both places—UAE and the other country where it happened. The AML/CFT regulations also include money laundering and related predicate offences in the definition of a crime. Ensuring compliance with these regulations is critical to avoid serious legal consequences.

Why Understanding Predicate Offences Matters

Predicate offences are the point of origin or source for Money Laundering activities. These offences generate proceeds that are later concealed through the act of laundering. Regulated Entities aiming to counter laundering risks must understand how underlying operations depend on these offences. A comprehensive understanding of relevant predicate offences is crucial, as the success of identifying and mitigating risks is dependent on this knowledge. Without the ability to fully comprehend these offences, managing and reducing financial crime threats becomes far more challenging.

Key Stages of Money Laundering and Related Predicate Offences

Money Laundering happens in three stages: placement, layering, and integration. In the placement stage, illegal proceeds from a predicate offence enter the financial system to conceal their illicit origin. Next, layering hides the laundered proceeds by transferring them across various accounts, making them harder to trace. Finally, in integration, the funds are merged into the economy, appearing as legitimate money. Sometimes, part of these funds is used to commit new predicate offences, creating a cyclical chain of crime that continues the process. This connecting link between offences and laundering makes it crucial to understand and prevent such activities.

Effects and Consequences of Predicate Offences

Predicate offences have a serious impact on businesses, institutions, and the entire economy. Vulnerable sectors face legal risks, operational risks, and social costs, such as damage to their reputation or a drop in credit score. Tax crime, fraud, insider trading, and market manipulation weaken the financial system, causing a loss of revenue for the government and reducing foreign investment. Additionally, money laundering risks, terrorism, and terrorism financing risks threaten national security and disrupt society. This increased exposure to crime affects the stability of a country, leading to long-term economic damage.

Regulatory Framework and Standards for Predicate Crimes

FATF Predicate Offences

The Financial Action Task Force (FATF) plays a vital role in defining and monitoring predicate offences. FATF sets AML/CFT standards that countries follow to fight money laundering and terrorist financing. Known as FATF’s 40 Recommendations, these guidelines act as the Northern Star, helping countries implement strong anti-money laundering measures. Among these recommendations is a comprehensive list of predicate crimes, covering a wide range of serious offences that can lead to laundering funds.

Designated Categories of Predicate Crimes

FATF classifies predicate offences into various designated categories, ensuring countries address the broadest possible range of illegal activities. These include felonies and misdemeanours that are often criminalised internationally. Examples include trafficking in human beings, migrant smuggling, extortion, and bribery. Financial-related crimes such as tax crimes (direct taxes and indirect taxes), insider trading, and market manipulation are also part of this list. Moreover, environmental offences like environmental crime and serious violent crimes such as murder, kidnapping, and grievous bodily injury are included as predicate crimes.

Common Predicate Offences in Money Laundering

Here are some of the most common predicate crimes according to FATF:

Corruption and bribery

Forgery and counterfeiting currency

Trafficking in narcotic drugs and psychotropic substances

Robbery, theft, and smuggling

Piracy and counterfeiting products

Organised criminal group activities and racketeering

Illegal restraint and hostage-taking

Trafficking in stolen goods

Each of these crimes provides an opportunity for criminals to launder funds through various channels, including customs fraud, excise duties violations, and counterfeiting products. Understanding and enforcing regulations for these offences is crucial to safeguard national and global financial systems.

EU Directives on Combating Money Laundering

The EU’s first directive set the foundation for fighting predicate offences, aligning with the 1988 Vienna Convention. It urged member nations to expand the scope to include other countries and crimes.

Global Framework for Regulating Predicate Offences

The global regulatory framework for Predicate Offences varies across countries due to differences in criminal codes and economy. In the UAE, Federal Decree-Law No. (20) of 2018 on Anti-money Laundering and Combating the Financing of Terrorism defines a predicate offence as any offence or misdemeanour under UAE laws. This applies whether the offence is committed within UAE or outside UAE, provided the principle of dual criminality is met. These regulations aim to address crimes that fund illegal organisations and protect the market from financial abuse.

UAE National Risk Assessment 2018: Focus on Predicate Offences

The UAE National Risk Assessment (NRA) in 2018 evaluated Money Laundering risks and identified several predicate crimes posing serious threats. Based on FATF 21 predicate offences, the assessment highlighted the following high-risk crimes:

Fraud

Counterfeiting and piracy of products

Illicit trafficking in narcotics

Professional third-party ML

Various other predicate crimes closely linked to Money Laundering activities

By identifying these risks, the NRA helps improve the country’s efforts to tackle financial crime and protect its economy.

How to Identify and Report Predicate Offences in the UAE

Identifying Predicate Offences in the UAE

In the UAE, Financial Institutions (FIs) and Designated Non-Financial Businesses and Professions (DNFBPs) must follow AML/CFT laws to detect and report predicate offences. Indicators like unusual transactional patterns or inconsistent financial status compared to business activities help identify potential risks. Cabinet Decision No. (10) of 2019 and Decree Law No. (20) of 2018 require entities to stay vigilant and report any suspicious transaction.

Role of the Financial Intelligence Unit (FIU)

The Financial Intelligence Unit (FIU) in the UAE monitors suspicious activities. FIs and DNFBPs must submit Suspicious Activity Reports (SAR) or Suspicious Transaction Reports (STR) through the goAML portal. This goAML Suspicious Transaction Reporting System ensures that suspicious activities related to ML/TF risks and Illegal Organisations are flagged and investigated.

Common Red Flags and Compliance

Compliance Officers help enforce internal rules and controls to reduce risks. They must track and update red flags regularly. Here are some common signs:

Transactions linked to high-risk jurisdictions

No clear source of funds explanation

Inconsistency between financial status and declared professional activities

Repeated unusual transactional patterns

Sudden involvement in high-value transactions without clear business justification

By closely following procedures and appointing a Compliance Officer, FIs and DNFBPs can better safeguard against financial crimes.

Key Challenges in Combating Predicate Offences

Investigative Challenges in Combating Predicate Offences

Financial Intelligence Units (FIUs) face difficulties in investigating predicate offences due to the intricate network of entities involved. Linking Money Laundering to a crime requires gathering reliable evidence and identifying complex connections.

Legal Complexities and Cross-Border Issues

The cross-border nature of predicate offences complicates investigations due to varying legal frameworks and jurisdictional complexities. Lack of mutual cooperation and bureaucratic delays further slow down efforts to tackle these crimes.

Evolving Threats with Technology

As technology advances, new threats like cybercrime and cryptocurrency-related crimes emerge, making it difficult for DNFBPs and FIs to detect suspicious activities. These sophisticated activities constantly evolve, challenging traditional monitoring systems.

Resource Constraints and Expertise

Many Regulated Entities lack the necessary resources and well-trained staff for effective AML compliance. This shortage hinders their ability to fulfil regulatory obligations and meet the required regulatory standards.

Key Focus Areas for Compliance

To address these challenges, DNFBPs and FIs should focus on:

Strengthening compliance programs

Training well-trained staff in AML compliance

Collaborating with regulatory authorities for mutual cooperation

Adapting to technology advances and monitoring suspicious activities

Allocating adequate resources to meet regulatory framework requirements

By implementing these strategies, entities can better manage the risks posed by predicate offences and illicit acts.

Liability for Predicate Offences under UAE AML/CFT Regulations

Under UAE AML/CFT laws, a person committing a predicate offence can also be found guilty of money laundering if they knowingly handle funds from an illicit source. Such individuals may be charged and punishable for both offences as independent crimes. This includes acts like hiding, transmitting, or possessing the proceeds of these crimes or helping other perpetrators escape punishment. The AML/CFT law ensures that offenders cannot avoid accountability, even if the crimes seem unrelated.

To safeguard against ML/FT threats, companies must build a robust AML framework. This requires skilful employees and knowledgeable employees to implement an effective compliance program. Regular AML training ensures senior management and staff have a consistent understanding of their role in detecting threats and protecting the company’s reputation. Key steps to strengthen your compliance strategy include:

Regular AML training for all levels, including senior management

Appointing skilful employees to oversee compliance

Creating a robust AML framework with clear reporting processes

Monitoring for ML/FT threats and unusual activities

Aligning with organisational objectives to promote a strong compliance culture

Effective Strategies to Combat Predicate Offences

1. Risk-Based Approach (RBA)

The Risk-Based Approach (RBA) helps Regulated Entities prioritize their AML compliance by applying stronger controls where ML risks are higher. The principle is simple—higher the risks, stronger the controls. This approach ensures better detection and mitigation at an early stage.

2. Customer Due Diligence (CDD)

Customer Due Diligence (CDD) involves collecting customer information, such as name, date of birth, nationality, and verifying it against official documents like a Driving License or ID Card. CDD ensures the legal nature of the customer’s business relationship is understood, reducing risks.

3. Know Your Customer (KYC)

KYC is an essential part of CDD. It requires DNFBPs and FIs to verify the customer identity by collecting relevant documents. This process helps ensure the customer is not involved in corruption, fraud, or drug dealing that could pose ML risks.

4. Name Screening

Name screening helps detect potential risks by matching customer details with Sanctions Lists, Politically Exposed Person (PEP) databases, and adverse media sources. This step is critical in identifying customers who may be involved in predicate offences or terrorism-related activities.

5. Risk Profiling and Assessment

Based on KYC and name screening, DNFBPs and FIs can classify customers into high-risk, medium-risk, or low-risk categories. Risk Profiling ensures that appropriate Enhanced Due Diligence measures are applied for high-risk customers.

6. Enhanced Due Diligence (EDD)

EDD is conducted for high-risk customers and involves collecting additional information, such as Source of Wealth and Source of Funds. Senior management approval is required before onboarding such customers to ensure thorough risk assessment.

7. Transaction Monitoring

Transaction monitoring is vital for identifying suspicious activities. DNFBPs and FIs must monitor transactions regularly to ensure they align with the customer’s transaction history and business relationship. Any unusual patterns should be treated as a red flag indicator.

8. Training and Awareness

Regular training for employees and senior management ensures a consistent understanding of AML compliance policies. This equips them to recognize suspicious transactions and implement internal procedures to combat predicate offences effectively.

9. Using AML Software

Modern AML software based on cutting-edge technologies helps address challenges like resource limitations and accuracy issues. These tools improve transaction monitoring and name screening, making compliance more efficient.

10. Collaborative Approach

A collaborative approach through public-private partnerships, information sharing, and transparency strengthens efforts to combat Money Laundering and predicate offences. Greater cooperation among stakeholders enhances detection and prevention.

Final Thoughts

A comprehensive understanding of predicate offences allows Financial Institutions (FIs) and Designated Non-Financial Businesses and Professions (DNFBPs) to strengthen control and reduce risks of money laundering and terrorism financing. This proactive approach ensures these entities can identify threats early and implement better prevention strategies for compliance and security.

FAQs

What is a predicate offence?

A predicate offence is a crime that leads to another serious financial crime, like money laundering or terrorism financing.

Why are predicate offences important in AML compliance?

Understanding predicate offences helps detect and prevent money laundering risks, enabling FIs and DNFBPs to implement stronger controls.

How do Financial Institutions (FIs) identify predicate offences?

FIs use Customer Due Diligence (CDD), name screening, and transaction monitoring to detect red flag indicators linked to predicate offences.

What role does a Risk-Based Approach (RBA) play in combating predicate offences?

The RBA ensures that entities focus their resources on high-risk areas, applying stronger controls to manage significant risks.

How can DNFBPs and FIs improve their AML compliance?

They can adopt AML training, use cutting-edge AML software, and build a robust AML framework to detect and mitigate ML/FT risks effectively.

Money laundering is a complex process in which criminals, initially, generate more illegal funds by hiding the origin of money gained from illegal activities like drugs, bribery, and human trafficking. The process begins, therefore, with the placement stage, where dirty money enters the financial system through transactions. Over time, criminals, consequently, use various techniques to bypass financial systems and rules, hiding the true source of the money.

Once the illicit funds are integrated, the money is made to appear legitimate. This is done by moving the funds through several layers of transactions and using other methods that make tracing difficult. It’s estimated that around $3.6 trillion is laundered globally each year, but law enforcement only seizes a small portion. By the end of the laundering process, dirty money is reintroduced into the economy, blending in with legitimate funds, often making it hard to spot.

The Chilling Stages of Money Laundering & Terrorist Financing

Money laundering is a criminal activity designed to conceal the origin of illicit funds. The first step, known as placement, occurs when dirty currency such as drugs, narcotics, or even digital currency enters the financial system. Money launderers often use methods like online payments or purchase luxury cars, jewelry, or real estate to make the illicit funds appear legitimate. The goal is to disguise black money, making it look like it has a lawful source.

First Stage: Placement

Next comes the layering stage. Here, money launderers hide the true nature of the funds by using complex transactions. They move money through various accounts and assets to blur the trail and make it hard to trace. This process also involves creating multiple layers of transactions, often using digital assets or illegitimate enterprises. Criminals may use pseudonymous tools to further hide their tracks and maintain anonymity.

Second Stage: Layering

The final step is integration, where money launderers, ultimately, aim to use the illicit funds for legitimate purposes. They may, for instance, invest in luxury goods like cars, real estate, or other high-value assets. By doing this, they aim to make the illicit funds appear clean. In this way, the goal is to seamlessly blend the illegal money into the economy, making it indistinguishable from genuine wealth.

Terrorist financing follows a similar path. Specifically, terrorist organizations often use donations, smuggling, and criminal activities like drug trafficking to fund their operations. Moreover, these funds are stored and moved through financial systems, art, and commodities to hide their illegal origin. In fact, both terrorist financing and money laundering rely on these complex methods to make it difficult for authorities to uncover the true source of the funds.

Techniques for Conducting the Placement Stage

Smurfing Technique

Smurfing is a method used by money launderers to break down dirty money into smaller, less noticeable sums. This is done by smurfs, who are individuals that help deposit the money into different banking accounts. These deposits often happen in cash-intensive businesses such as casinos, convenience stores, or laundromats. The goal is to make it hard for financial institutions to track these transactions and stay under the reporting thresholds like the $10,000 mark.

Structuring Process

Structuring is quite similar to smurfing, but it focuses more on avoiding scrutiny by making smaller cash deposits across multiple accounts, bypassing the financial regulations meant to flag large sums. By staying just under $10,000, the launderers can launder money while evading detection. This method is common among money launderers who want to stay under the radar and avoid financial crime alerts.

Using Shell Companies

Another technique used is setting up shell companies, which are fake businesses that are created just for this purpose. Money launderers deposit dirty money into these fake businesses, and then transfer it to a real business. This helps make the funds look legitimate and blend in with the legitimate revenue of the real business. The ease of doing this increases in areas with weak financial regulations or weak compliance.

Cryptocurrency Transactions

With the rise of cryptocurrency, money launderers have, consequently, found ways to use cryptocurrency for laundering money. Bitcoin ATMs and unregulated exchanges are commonly used, as they allow launderers to buy crypto using dirty money. In 2022 alone, approximately $23.8 billion in cryptocurrency was transferred through illicit addresses. This process is often, in fact, done through peer-to-peer transactions, where crypto is exchanged for cash or vice versa.

High-Value Purchases

High-value purchases like luxury cars, jewelry, or real estate are often used to introduce dirty money into the financial system. Launderers first buy these items with cash, then resell them, receiving payments electronically. This method is a popular way to make illicit funds appear as legitimate legitimate cash, and it helps launderers blend their dirty money into the financial economy.

Cash-Based Businesses

Cash-based businesses, such as bars, restaurants, or laundromats, are ideal for money launderers. The influx of legitimate cash helps mix in the dirty money without raising suspicion. As a result, it becomes increasingly difficult for financial institutions or law enforcement to trace the origin of the illegal funds.

Consequences of the Placement Stage

Weakening Financial Systems

Money laundering weakens financial institutions, making them vulnerable to abuse and criminals. This undermines the integrity of the financial systems and can cause long-term damage to economic growth and public trust.

Increased Reach of Criminals

Laundered money helps criminals fund dangerous crimes and terrorism, increasing their reach. This impacts society’s stability and puts everyone at risk.

Impact on Financial Stability

When illicit funds infiltrate the system, financial vulnerability rises, causing more economic growth challenges. This leads to destabilizing effects that threaten the safety and well-being of society.

Final Thoughts

Understanding how money laundering works is essential for protecting the integrity of global financial systems. Launderers use various methods to place funds and funnel illicit money into legitimate systems. The main goal, ultimately, is to hide the illegal nature of the funds. By doing this, they, therefore, make it harder to detect. Financial systems, as a result, need to fight these activities to maintain their stability. This fight, in fact, includes tackling terrorist financing and organized money laundering, which are widespread problems. To stop this, it’s crucial, above all, to understand these techniques and address the pervasiveness of the issue.

In the UAE, trusts and corporate service providers (TCSPs) manage legal persons and legal arrangements. However, they face high risks of money laundering (ML) and terrorism financing (FT). To combat these risks, authorities enforce AML and CFT laws with stringent compliance requirements. A trustee, secretary, or partner involved in creation, establishment, or directorship must perform proper due diligence. This step prevents the misuse of money and ensures accountability. If firms ignore regulations, they risk engaging in suspicious transactions with other countries where oversight is absent. As a result, their exposure to financial crime may increase.

Here are the key AML and CFT requirements:

Maintain a registered office, work address, or administrative address to ensure transparency in dealings.

Prevent the abuse of corporate vehicles by monitoring correspondent addresses and nominee shareholders.

Strengthen collaboration with financial services to detect and prevent high-risk activities.

Identify and report suspicious transactions linked to financers or illicit financial activities.

Ensure every agent involved in company structuring follows strict conduct guidelines.

Comply with regulatory requirements to prevent exposure to absent controls in other countries.

Regularly update internal policies to address new AML and CFT threats.

By following these rules, TCSPs and trusts in the UAE can protect their businesses and meet AML and CFT compliance standards.

Suspicious Transactions Indicating ML/FT Risks in TCSPs

How TCSPs Can Identify and Prevent Financial Crimes

In the UAE, TCSPs manage business relationships and handle legal entities, making them targets for ML/FT risks. These risks exist at both enterprise and customer levels. Some clients try to hide their beneficial ownership using nominee agreements, while others provide fake identity documents or wrong addresses. Additionally, businesses may use third-party transactions with an unknown identity or an unusual payment method to avoid detection. Without strict monitoring, these arrangements can result in criminal transactions and movement of illicit funds through unauthorized transactions. Furthermore, companies based in tax havens or regions with high corruption, terrorist organizations, and a weak AML/CFT regime pose significant debt and country risks to financial systems.

To prevent financial crimes, watch for these red flag indicators:

Clients creating complex company structures to engage in layering and conceal illicit funds.

Businesses involved in multiple invoicing, over-invoicing, or under-invoicing to manipulate transaction records.

Firms conducting excessive cash transactions or holding disproportionate funds without clear financial backing.

Entities with high levels of assets but frequently changing their organizational structure.

Clients avoiding direct payments, instead using a third party with an unknown identity.

Companies linked to PEPs, individuals under sanctions, or firms operating in tax havens.

Use of bribes to bypass regulations and conduct illegal transactions through accounts.

To stay compliant with AML and CFT laws, TCSPs must track these transaction risks and enforce strong accounting controls. Proper oversight helps prevent financial crimes and ensures regulatory compliance.

AML Compliance Rules for Trusts & Corporate Service Providers in the UAE

In the UAE, TCSPs must follow strict AML compliance measures to prevent financial crimes. The Decree-Law No. 20 of 2018 on Anti-Money Laundering and Combating the Financing of Terrorism sets the foundation for regulating business relationships and financial transactions. Additionally, Cabinet Decision No. 10 of 2019 provides an Implementing Regulation to guide companies in following AML/CFT programs. These rules require firms to establish internal policies, apply customer due diligence, and implement clear procedures. This helps detect suspicious transactions and reduce risks associated with money launderers and financial criminals.

To enhance protection against fraud, TCSPs must comply with strict regulations and maintain a strong governance framework. They must also report any suspicious transactions and verify that their clients meet legal standards. These obligations help identify Illegal Organizations, prevent fraud, and ensure compliance in financial activities. By following these provisions, firms can minimize ML and FT risks while securing the financial system.

Essential AML/CFT Compliance Guidelines for Trusts & Corporate Service Providers in the UAE

Trusts and corporate service providers must adhere to these essential requirements under the AML regulations in the UAE:

Identifying Potential ML/FT Risk Exposure

Understanding exposure to ML and FT is essential for TCSPs to follow AML/CFT measures and prevent financial crimes.

Review business relationships, client risks, and complexity of financial transactions to spot potential threats.

Examine the country of origin, country of operations, and geographical sources to detect risks from a foreign client.

Monitor channel risk, preferred mode of communication, and financial arrangements to identify any unusual nature of dealings.

Apply a risk-based approach, maintain proper documentation, and assign a risk rating for efficient management and compliance.

Enforce Customer Due Diligence Procedures

To prevent financial crimes, TCSPs must apply strict customer due diligence (CDD) measures. Verifying a client’s identity and checking their background information helps ensure compliance and reduce ML and FT risks. Screening against Sanction lists can reveal connections to PEPs, money launderers, or third-party intermediaries. Additionally, businesses must assess financial transactions, business activities, and legal arrangements to uncover hidden risks.

Conduct a thorough assessment of the client profile to detect irregularities in acquisition, transfer, or financing activities.

Verify the beneficial owner using independent sources and investigate hidden ownership through proxies or complex structures.

Scrutinize legal arrangements that appear opaque or involve excessive influence over business operations.

Perform regular screening of clients and partners to ensure reliability in financial transactions.

Maintain continuous scrutiny of financial instruments to identify unusual transactions and potential risks.

Establish Internal Policies, Controls, and Compliance Procedures

To minimize ML and FT risks, trusts and company service providers must establish strong and effective internal policies. These policies should include customer due diligence, suspicious transaction reporting, and record-keeping. Additionally, maintaining proper governance and structured procedures ensures legal compliance and supports risk mitigation. Conducting regular assessments keeps policies updated and aligned with regulatory requirements.

Organizations must focus on the implementation of strict controls to strengthen risk management. Routine updates are necessary to address new threats and evolving compliance rules. Applying effective measures enables businesses to meet AML and CFT standards while securing financial operations.

Notify the Financial Intelligence Unit (FIU) About Suspicious Transactions

Businesses must report suspicious transactions to the Financial Intelligence Unit (FIU) to prevent AML and CFT violations. Monitoring risk profiling and identifying unexplained transactions ensures compliance. Any complex transactions with an unknown beneficial owner or unclear sourcing of funds should raise concerns. Companies must exercise vigilance and keep updates on every alleged transaction.

Report suspicious transactions linked to high-risk countries or involving an unrelated third party.

Flag ownership changes that lack a clear reason or involve hidden entities.

Investigate dubious transactions that do not align with the client’s income or turnover.

Ensure due diligence measures are followed when verifying proofs of financial activity.

Watch for customer refusal to provide relevant information required for compliance.

Submit reporting on all unusual activities that may suggest financial misconduct.

Track and document involvement in transactions that seem fraudulent or excessive.

Continuous Oversight

TCSPs must perform monitoring to prevent money laundering and financial crimes in their business relationships. Regular detection of unusual patterns in transactions, transfers, and payments helps identify risks early. Any inconsistencies in a client’s profile, identity, or history should be verified through registries to ensure accuracy.

Track frequency, size, and amount of transactions to detect unusual financial behavior.

Verify third-party accounts, foreign accounts, and unknown sources to prevent financial fraud.

Stay alert for clients from high-risk countries or linked to PEPs, especially before account closure or during the account life cycle.

Conclusion

For TCSPs and company service providers in the UAE, following AML and CFT regulations is crucial to minimizing risks. A strong fight against money laundering begins with proper due diligence, accurate identification, and strategic management of business relationships. Recognizing terrorism financing risks and using best practices can help prevent fraudulent transactions and reduce exposure to financial crime.

Collaborating with AML consultants provides professional, industry-specific support for implementation. Keeping up with international regulations, global regulations, and national measures enhances financial security. Trusts and service providers must regularly improve their compliance strategies to maintain financial stability and integrity.

Importance of AML Regulations in the UAE

Ensuring AML and CFT compliance is essential for businesses operating in the UAE. A well-structured AML compliance department helps companies implement internal controls, follow guidelines, and meet global regulations. Proper risk profiling and CDD measures reduce financial risks while improving business operations. Using AML software enhances screening and filing processes, ensuring adherence to national boundaries and best practices.

Assist in the selection and submission of risk assessment reports to the UAE government.

Conduct training for employees on KYC, EDD, and financial crime prevention.

Ensure effective implementation of procedures and firm-specific policies.

Manage AML-related activities through structured STRs filing and monitoring.

Engage an expert team for conducting audits and ensuring legal compliance.

Frequently Asked Questions (FAQs)

1: Why is sanction screening and PEP screening important in the onboarding process?

Sanction screening and PEP screening help detect high-risk customers and prevent money laundering. These checks ensure transparency in financial dealings and stop criminals from misusing client accounts. By identifying illicit funds and suspicious assets, businesses can follow AML/CFT regulations and maintain compliance.

2: What is the role of a compliance officer in AML/CFT compliance?

A compliance officer oversees internal policies, procedures, and controls to ensure adherence to AML/CFT regulations. They conduct audits, perform reviews, and suggest improvements where needed. Their duties include training compliance staff, assessing proficiency, and ensuring businesses operate with diligence.

3: How do TCSPs and trusts face risks of money laundering?

TCSPs and trusts are at risk when clients lack transparency, engage in unusual transactions, or attempt to hide ownership of legal entities. Criminals may use these services for capitalization, acquisition, or transferring proceeds from illicit funds into the financial system. To mitigate these risks, businesses must monitor legal arrangements and restrict unauthorized access.

Many people think Know Your Customer (KYC) and Anti-Money Laundering (AML) are the same, but they differ in key ways. KYC helps financial institutions verify customer identities and meet legal obligations set by national and international authorities. Meanwhile, AML regulations focus on preventing money laundering by adding strict monitoring and screening measures. These terms are often used interchangeably, causing confusion in their context.

However, their importance in financial compliance is undeniable. Since both are mandated processes, firms must have strong familiarity with their functions. Understanding their role in regulatory procedures ensures smooth business operations and prevents legal risks.

AML vs. KYC: Key Differences Explained

Both AML and KYC help financial organizations prevent financial crimes, but they serve different purposes. KYC focuses on identifying customers by requiring businesses to collect key information like name, address, date of birth, and incorporation documents. It also includes customer screening checks, such as politically exposed person (PEP) screening, sanctions screening, and adverse media screening to reduce risks.

On the other hand, AML measures go beyond identity verification. They include transaction monitoring, an ongoing process used by companies to track unusual financial behavior. These checks help businesses verify identities and follow strict regulatory requirements. By combining KYC and AML, financial institutions create a strong defense against fraud and illegal transactions.

Inside the AML Screening Process: What Happens Step by Step?

How the AML Screening Process Works

The AML screening process begins with assessing customer data to determine their risk level. Financial institutions focus on identifying high-risk customers by evaluating their source of funds, geographical location, and any history of criminal activities. If a customer has been involved in money laundering or shows suspicious activity, they are flagged for further review.

Once the risk is determined, a monitoring process is put in place to track transactions. Institutions watch for sudden changes in account activity, large transfers, or dealings in high-risk jurisdictions. If anything unusual happens, it is reported to the appropriate authorities to ensure compliance with AML regulations. This ongoing activity includes continuous tracking and monitoring to detect financial crimes early.

KYC Process Explained: How It Works Step by Step

How the KYC Process Works

To follow AML regulations, financial institutions ask new customers to provide a valid passport, driver’s license, or other documents to prove their identity. Once the customer information is collected, it is verified through third-party sources like credit bureaus, government records, or banks. After verification, institutions store the data in a secure database and monitor customer activity to detect any suspicious or fraudulent activity. If needed, customers must submit additional documents to fully comply with regulations.

KYC, CDD, and EDD: Understanding the Key Differences

KYC follows a risk-based approach to help firms identify customers and assess their money laundering risk. The first phase involves collecting customer information during the onboarding process. In the second phase, businesses verify this data using independent source documents like passports, ensuring it meets standard due diligence requirements. A customer risk rating is then assigned based on risk levels. If a customer is low risk, they undergo standard CDD measures, which include verifying their beneficial owner and checking that transactions match their profile.

If a customer is high-risk, they require Enhanced Due Diligence (EDD). This process includes additional customer identification materials, verifying the source of customer funds, and scrutinizing transactions for irregularities. Businesses must also apply intensive AML scrutiny to ensure transactions align with legal requirements. Ongoing monitoring procedures and due diligence steps are necessary to determine whether a business relationship should be pursued or maintained. The Financial Action Task Force (FATF) recommends these procedures, which involve monitoring transactions on an ongoing basis and ensuring they are conducted under legal assessment. Every act, claiming to be authorized, is verified to prevent fraud. The primary goal of these processes is to strengthen financial security and compliance.

Where Are AML and KYC Solutions Essential?

Many firms across different jurisdictions must implement an AML program to fight financial crime and follow AML regulations. These programs should be tailored to meet business needs while addressing specific risks within different business sectors.

As financial threats grow, prevalent trends shape how companies manage compliance. Effective monitoring processes and practical screening methods must align with AML legislation and meet the requirements of financial authorities. To stay compliant, organizations must update their monitoring systems regularly to match legislative needs and protect their customers.

When Should KYC Measures Be Implemented?

The KYC process begins during onboarding to confirm that customers provide truthful information about their identity and financial activities. Identity verification involves an assessment of personal information, ensuring the legitimacy of an individual or entity. If an organization is acting on behalf of someone else, firms must establish the beneficial ownership of that business.

However, KYC is not a one-time process. It continues throughout the business relationship to track any potential risks. Companies frequently review a client’s risk profile to ensure it still matches the previous assessment. This helps detect changes in business relationships and prevents financial fraud before it happens.

Adapting KYC for Stronger AML Compliance

The rise of FinTech innovations and digital disruptors has changed how financial institutions handle KYC controls to meet regulatory compliance. Challenger banks and mobile banking have reduced onboarding times, but also introduced negative effects, such as increased false positives and human error in identity verification.

To improve compliance performance, businesses now use specialized KYC software and automated requests to collect customer data efficiently. Biometric KYC, including fingerprints and voiceprints, helps verify high-risk customers while refining risk profiles.

The Wolfsberg Group emphasizes using advanced data analysis and artificial intelligence to detect criminal methodologies and enhance risk mitigation. As financial threats evolve, businesses must adapt their AML program to comply with government authorities, reduce fraud, and meet ongoing regulatory responsibilities in a complex compliance environment.

In today’s world, proliferation financing (‘PF’) is a growing global threat that fuels the spread of WMD programs. It involves raising and making available funds, assets, and other economic resources to dangerous entities. These groups engage in the development, manufacture, and export of nuclear, chemical, and biological weapons. Countries like North Korea and Iran remain under Targeted Financial Sanctions (‘TFS’) due to their ongoing acquisition and stockpiling of proliferation-sensitive materials. Criminal networks disguise the funds through money laundering, making it harder to stop illegal transfers.

To operate, these groups misuse Dual-Use technologies and exploit DNFBPs (Designated Non-Financial Businesses and Professions). They use them for brokering, transport, and trans-shipment of related materials. The process happens in stages, starting with program fundraising, followed by concealing transactions, and ending in the proliferation of their means of delivery. The use of these materials for non-legitimate purposes threatens global society and security. Because their tactics keep evolving, stopping proliferation financing requires strong regulations and global cooperation.

Proliferation Financing Risk: A Looming Global Danger

The proliferation financing risk is a serious threat that fuels the spread of WMD. To fight this, DNFBPs must assess risks and adopt strong measures for mitigation. Any breach, evasion, or non-implementation of TFS obligations weakens financial security. That is why the United Nations Security Council Resolutions focus on prevention, suppression, and disruption of illegal financing tied to proliferation. Without strict regulations, these risks will continue to grow.

PF Risk Assessment: A Critical Pillar of AML/CFT Policy

To effectively assess PF risk, DNFBPs must first understand the following key aspects:

The Alarming Threats of Proliferation Financing

The risk of Proliferation Financing (PF threats) is increasing as criminal entities continue to exploit financial systems. It is widely assumed that terrorist groups and rogue countries, such as North Korea and Iran, seek nuclear weapons and radiological materials. A breach in financial regulations or a failure to implement strict TFS controls allows these actors to evade detection. This ongoing risk poses a serious threat to global peace and security.

Hidden Vulnerabilities That Fuel Proliferation Financing

Different sectors face vulnerabilities that make them attractive to illegal financing. Weak DNFBPs oversight, gaps in banking and insurance, and unregulated virtual assets facilitate hidden transactions. Additionally, money transfer services in high-risk jurisdictions, like Iran, allow evasion and non-implementation of TFS measures. To reduce these risks, UAE authorities rely on international reports and PF typologies to identify weak points. Sectoral reports further assess risks within various business structures and financial products.

Devastating Consequences of Proliferation Financing

Weak financial controls have serious consequences, enabling proliferators to procure dangerous materials for developing illicit biological weapon systems and other destructive tools. Misused funds and assets contribute to the rise of WMD, increasing the threat of their use. If left unchecked, these systems could cause devastating global instability.

Proliferation Finance Risk Assessment: A Critical Shield

To fight PF risk, DNFBPs must clearly understand their exposure and apply a structured assessment process. Their approach should match the nature and size of their business, ensuring proper risk management. A well-documented PF risk assessment should classify threats into key categories and highlight vulnerabilities. Keeping an updated document helps organizations strengthen compliance and prevent financial misuse.

Geographic Hotspots That Drive Proliferation Financing

Detecting geographic risk is crucial to stopping PF risk, as criminals use hidden global networks to move money illegally. North Korea and Iran rely on neighbouring countries and indirect routes to acquire proliferation materials. DNFBPs must assess their business locations and target markets to prevent illegal financial activity. If left unchecked, these risks can benefit terrorist groups and fund dangerous operations.

High-Risk Customers in Proliferation Financing

Understanding customer risk helps stop illicit transactions. DNFBPs should screen UN-sanctioned individuals and entities listed on the TFS list. Identifying the UBO of companies involved in proliferation-sensitive goods is critical. The CDD process should review a client’s business place, residence, and geographic connections. If a sanctioned person engages in suspicious customer business activities, financial institutions must act quickly to reduce PF risk.

Weaknesses in Products and Services That Enable Proliferation Financing

Financial services and products can be exploited to fund WMD activities. Institutions should assess how their services may be used to disguise transactions or obtain proliferation-sensitive goods. DNFBPs must apply strict risk controls to stop criminals from misusing funds for proliferation financing. Strong oversight prevents illegal networks from taking advantage of financial loopholes.

Effective Strategies to Prevent and Reduce Proliferation Financing Risk

DNFBPs should identify and monitor high-PF risk customers, especially those linked to high-risk jurisdictions like Iran and North Korea.

Conduct Enhanced Due Diligence (‘EDD’) on customers categorized as sanctioned or involved in proliferation financing to detect suspicious activities.

Always check and inquire about the TFS policy of clients to ensure compliance with financial regulations.

Secure approval from senior management before processing any business transaction with listed high-risk customers.

Establish a strict policy to restrict dealings with customers from high-risk jurisdictions to prevent illegal financial activities.

If a possible PF activity is envisaged in a transaction, freeze the funds and report it immediately using the goAML Portal.

Verify the ultimate beneficial owner of an entity to prevent financial misuse or illegal trade of goods.

Watch for red flags, such as unknown end users or unclear business dealings, that may indicate financial crimes.

Sanction Evasion and PF Red Flags

Dealings with sanctioned countries, territories, or sanctioned persons through a DNFBP’s client can indicate illegal financial activity.

The use of shell companies to move funds locally and internationally often leads to misappropriating the commercial sector for unlawful purposes.

Transactions involving sanctioned goods or Dual-Use goods should be carefully reviewed to prevent illegal trade.

Fake or altered identifying documents, such as a bill of lading or sales purchase agreement, may be forged, counterfeited, or tampered with.

If there is no apparent explanation for document changes in international trade, further investigation is necessary.

A financed activity that does not match the original purpose or intended purpose of the entity could signal fraud.

Companies importing high-end technology devices without the proper trade license raise serious concerns.

A non-profit organization exporting communication devices instead of offering humanitarian aid may be engaged in illicit activities.

Complex commercial deals or business deals designed to hide the final destiny of a transaction or good may indicate sanction evasion.

Complex legal entities and arrangements created to obscure the beneficial owner should always be examined for suspicious activity.

Critical Insights from the EOCN Survey on Global Security and Proliferation Control

The Executive Office for Control & Non-Proliferation (‘EOCN’) conducted a survey to measure awareness of Proliferation Financing, TFS, and Sanctions Evasion Techniques among reporting entities in the UAE. This survey helped assess DNFBPs’ understanding of PF-risk mitigation, compliance status, and risk assessment. It focused on key areas such as:

How businesses detect red flags linked to PF risk and financial crimes.

When to freeze funds in suspicious circumstances to prevent illegal transactions.

The need for screening high-risk customers and associated parties to spot possible proliferators.

How DNFBPs should follow PF guidelines and implement policies to stop financial crime.

The role of a Compliance Officer in preventing evasion of sanctions.

The value of trainings on UNSC sanctions and financial security measures.

These insights will help authorities improve regulations and ensure reporting entities follow strict compliance standards.

AML UAE: Your Trusted Financial Shield

To meet UAE authorities and United Nations Security Council regulations, DNFBPs must have a clear PF policy to detect and mitigate proliferation financing risks. This policy should be integrated with the AML/CFT Policy to enhance financial security. Businesses should assess their existing policy, follow a structured risk assessment process, and align with UAE requirements and international requirements. A strong understanding of these obligations helps prevent financial crimes and ensures compliance with global standards.

FAQs:

1. What is a PF policy, and why is it important?

A PF policy helps detect and mitigate risks related to proliferation financing. It ensures businesses comply with UAE authorities and United Nations Security Council regulations.

2. How does a PF policy connect to AML/CFT Policy?

A PF policy should be integrated with the AML/CFT Policy to strengthen financial security and prevent illegal financial activities.

3. Who is required to implement a PF policy?

All DNFBPs must follow a PF policy to meet UAE requirements and international requirements, ensuring compliance with financial regulations.

4. What is the purpose of a risk assessment process?

The risk assessment process helps businesses identify and evaluate proliferation financing risks, making it easier to implement preventive measures.

5. How can businesses ensure their PF policy meets compliance standards?

Companies should assess their existing policy, update their procedures, and align them with UAE requirements and global financial laws.

6. What are the consequences of non-compliance?

Failure to follow PF policy regulations can lead to fines, legal action, and reputational damage, affecting business operations.

7. How can businesses stay informed about PF regulations?

Companies should review their PF policy, attend training, and stay updated on United Nations Security Council financial crime regulations.

What if criminals could secretly move illegal money without setting off alarms? This is exactly how smurfing works—a deceptive money laundering technique where large amounts of cash are broken down into smaller amounts and deposited into multiple accounts. The purpose is to stay under the radar and avoid detection by banks. By staying below legal thresholds that trigger reporting, criminals can move money unnoticed. Unlike conventional laundering, which may involve a single individual, smurfing often requires multiple individuals or even entire organized crime groups. These criminals manipulate transaction values to make illegal activities look normal. As a result, financial institutions struggle to identify suspicious transactions, allowing devastating consequences for banks, businesses, and society as dirty money circulates freely.

To prevent smurfing, financial institutions must improve identification and tracking systems. Criminals take advantage of weak regulations and poor monitoring to keep moving funds without raising suspicion. However, by strengthening fraud detection tools, banks can safeguard themselves from financial crimes. If smurfing is not controlled, it empowers crime groups to expand their operations. Understanding structuring and how criminals exploit it provides crucial insights into stopping financial fraud before it escalates.

What Is Smurfing & How It Threatens Financial Institutions?

Criminals use smurfing to secretly move illegal funds into the valid financial system without drawing attention. They do this by splitting a large sum of cash into smaller amounts and making multiple transactions under the AML reporting threshold. This strategy helps them avoid suspicion, making it harder for banks to detect fraud. When detection is weak and the applicability of AML measures is poor, criminals easily facilitate the placement of dirty money into legal accounts. To fight this, financial institutions and regulatory authorities must strengthen monitoring systems and close loopholes that threaten the economy.

The Impact of Smurfing on Financial Institutions

Smurfing poses a major risk to financial institutions by allowing criminals to launder the proceeds of criminal activities without drawing attention. Banks and other institutions, whether knowingly or unknowingly, may facilitate illegal transactions, leading to a breach of their regulatory obligation. If they fail to act, they face legal consequences, including heavy fines for AML non-compliance. Weak controls and the absence of robust procedures make it easier for criminals to misuse the system. When financial institutions do not identify and prevent suspicious activities, they indirectly support financial crime, damaging the industry’s integrity and security.

The exploitation of banks through smurfing leads to severe damages, such as the loss of public trust and harm to their reputation. Once linked to money laundering, a financial institution struggles to regain credibility. Regulators demand strict reporting and compliance to curb financial crimes. To mitigate these risks, institutions must design and implement effective fraud detection systems and strengthen transaction monitoring. Establishing strong policies and conducting proper training can prevent them from aiding illegal money transfers. Taking proactive steps is essential to stopping the entry of illicit funds and protecting the financial system.

Common Smurfing Techniques Used in Money Laundering

Criminals use smurfing techniques to break a large cash amount into smaller deposits or withdrawals across multiple accounts at different financial institution locations. By spreading transactions across various branches, they make it harder for banks to spot illegal activity. Some use wire transfers and other electronic means to move money discreetly. Others open accounts under multiple individuals to conduct transactions without drawing attention. The goal is to avoid AML scrutiny while transferring illicit funds.

Banks must monitor for suspicious patterns, such as repeated fund transfers of the same amount from different accounts or withdrawals made simultaneously under one same beneficiary. Increased awareness of customer tactics and close tracking of customer behaviour can help stop financial crime before it spreads.

Cuckoo Smurfing: A Deceptive Tactic in Money Laundering

Cuckoo Smurfing is a secret money laundering method that criminals use to move illegal funds through regular banking channels without detection. This step-by-step process involves transferring money by tricking innocent account holders and disguising transactions as normal deposits. One of the key elements of Cuckoo Smurfing is using unsuspecting individuals to receive and send money, making transactions seem legitimate. Banks and financial institutions should watch for indicators such as unusual deposits, mismatched sender and receiver details, and repeated transfers of similar amounts. Identifying these warning signs early can help stop financial crimes before they escalate.

Understanding the Cuckoo Smurfing Method in Money Laundering

Cuckoo Smurfing is a secret money laundering method where criminals exploit bank accounts of legitimate customers expecting funds from overseas. They split large transactions into smaller amounts to stay below the regulatory threshold and avoid reporting to the FIU. By comingling illicit money with legal transfers, they disguise the illicit proceeds as funds from a legitimate source. This scheme is named after cuckoos that lay eggs in the nests of other birds, tricking them into raising foreign offspring. Similarly, victims remain unaware that they are handling proceeds of crime. Money transfer agents unknowingly assist in moving illegal funds, making this process difficult to detect.

Key Elements of the Cuckoo Smurfing Method in Money Laundering

Cuckoo Smurfing moves illicit money without a physical transfer, making detection harder for authorities. This scheme relies on cross-border transactions, where the transferor and beneficiary are in different countries. Criminals use structuring to split large amounts into smaller amounts, keeping deposits under reporting thresholds to avoid suspicion. The involvement of Smurfs is key, as they deposit cash into the bank account of an unaware legitimate customer. These transactions often hide funds from illegal activities, creating serious risks for financial institutions.

Step-by-Step Process of the Cuckoo Smurfing Method

Role of the Overseas Transfeor and Remitter

The overseas transferor starts a cross-border money transfer and deposits funds with a remitter instead of sending money directly.

To hide the illegal transaction, the remitter contacts a professional money laundering syndicate in the recipient’s country.

The syndicate deposits cash into the bank account of the beneficiary, making the transaction look legitimate.

Once the money is transferred, the remitter repays the syndicate using secret methods to disguise the transaction.

How the Beneficiary is Used in the Process

The professional money laundering syndicate deposits small amounts to avoid reaching the reporting threshold set by financial institutions.

Criminals use structuring to break down transactions, making them harder to detect.

The beneficiary believes they received money from the overseas transferor, similar to how a Cuckoo’s Nest tricks other birds.

In reality, the money comes from illicit sources, helping criminals move illegal funds without raising suspicion.

Warning Signs of Cuckoo Smurfing

Financial institutions and other reporting entities have legal obligations to detect suspicious transactions that may indicate cuckoo smurfing. Some red flags include repeated small deposits from unknown sources, mismatched sender and recipient details, and unusual transaction patterns. If a bank identifies such activities, it must submit a Suspicious Activity Report or a Suspicious Transaction Report to authorities. Detecting these warning signs early helps prevent financial crimes and protects the banking system from fraud.

1: Cuckoo Smurfing: Key Demographic Warning Signs

Cash deposits often occur at remote ATMs with less surveillance, making it harder for authorities to track suspicious activity.

Criminals make cash deposits at a different location instead of the home location of the beneficiary to avoid suspicion.

Transactions take place at multiple bank branches and ATMs on the same day, raising concerns about money laundering attempts.

Deposits are made in quick succession at the same location, making the activity look highly unusual.

Large amounts are structured into smaller cash deposits at a bank branch and ATMs to bypass monitoring systems.

2: Cuckoo Smurfing: Key Account Warning Signs

A beneficiary who is an unemployed person, student, or retired person receives frequent cash deposits without a clear source of income.

Multiple cash deposits happen in quick succession, structured to stay under the reporting threshold to avoid suspicion.

Deposits are made through ATMs using a single card, but funds are linked to multiple beneficiaries, which raises red flags.

The amount deposited does not match the customer’s profile, making the transaction appear unusual.

Cash deposits in the account align with an international fund transfer, making the transaction pattern questionable.

The account follows an instruction to move money soon after deposits, suggesting possible money laundering activity.

3: Understanding Cuckoo Smurfing in Money Laundering

A depositor makes cash deposits into multiple beneficiary accounts, which raises suspicion about whether the transactions are legitimate.

The same person repeatedly initiates cash deposits into a beneficiary account from a distant location, which is unusual behavior.

Multiple depositors use the same beneficiary details and make frequent cash deposits, a common sign of Cuckoo Smurfing.

The depositor’s name appears fictitious, suggesting an attempt to hide the true source of the funds.

A sudden increase in cash deposits across unrelated accounts, with no clear business purpose, may indicate possible money laundering.

Effective Ways to Detect Cuckoo Smurfing

Verify the relationship between the depositor and the beneficiary to confirm if the transactions are genuine or suspicious.

Check if the beneficiary is aware of the cash deposits or the fund transfer from an overseas account.

Ask the remitter about the source of funds to ensure they are not linked to illegal activities.

Identify any suspicious transactions made by third-party depositors who have no clear connection to the account holder.

Review video footage to spot unusual deposit patterns and investigate individuals involved in questionable financial activities.

Best Practices for Entities to Prevent Cuckoo Smurfing

Business entities should take steps to protect themselves from cuckoo smurfing by using legitimate financial institutions and trusted money exchange houses for transactions. They must monitor their bank account regularly for unexpected bank deposits or unusual transaction patterns. If they notice any suspicious activity, they should report it immediately to the authorities. Using reliable financial services and staying alert can help businesses avoid involvement in illegal money laundering schemes.

Regulatory Measures to Combat Smurfing in Money Laundering

The AML regulatory framework helps financial institutions detect and prevent money laundering, especially smurfing. These institutions need to understand the risk of smurfing and follow the guidelines set by regulations to avoid financial crimes. By following these rules, they can implement effective measures and remain compliant with laws against illegal activities. Complying with these regulations is crucial to preventing financial fraud and keeping the financial system secure.

Anti-Money Laundering Regulations to Combat Smurfing

The AML regulations in the UAE require financial institutions to adopt strong procedures, controls, and systems to identify and prevent money laundering. This includes addressing smurfing, a method often used to move illegal funds through suspicious activities. Institutions must assess the risk of smurfing and create a robust AML framework to tackle these threats. By following these policies, they ensure their systems can detect and handle unusual transaction patterns.

To catch smurfing, financial institutions need advanced monitoring systems with algorithms and Artificial Intelligence. These systems detect suspicious activity by analyzing transaction data for financial behaviour that doesn’t match a customer profile. Alerts are triggered when transactions differ from a customer’s usual activities, helping to spot illegal behavior.

Along with monitoring transactions, regular periodic reviews of customer information and customer due diligence are crucial. Financial institutions must update risk assessments regularly. This ensures compliance with AML regulations and helps spot discrepancies that could indicate suspicious activities or attempts to launder money via smurfing.

KYC and CDD Policies to Prevent Smurfing